Why do you need Retirement Planning

Here are reasons why retirement planning in India is pretty essential during the early years:...

Continue Reading

Here are reasons why retirement planning in India is pretty essential during the early years:...

Continue Reading

Don't spend too much time on deciding where, how and when to invest. The faster you invest money, the more it earns.

Continue Reading

In general, our investing decisions are shaped by the following factors.1. Having herd mentality When people watch their neighbors, friends...

Continue Reading

When selecting a mutual fund, an investor has to make an almost endless number of choices.

Continue Reading

First time mutual fund investors are often confused about the concept of Net Asset Value (NAV) of a mutual fund scheme.

Continue Reading

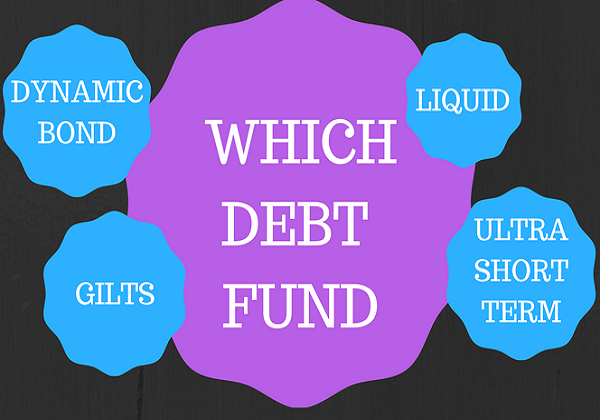

Schemes which do not invest in Equity or Equity related instruments are termed as Debt Funds, These funds do not invest in share market...

Continue Reading

Investing is not just about picking winners, but also about avoiding mistakes. Retail investors can be better off if they avoid making the following mistakes.

Continue Reading

Here are a few personal finance tips that young professionals would well to be aware of...

Best mutual fund scheme does not mean the best in returns, but the one best suited to your

risk profile and goals and the one that is good in its peer group.

A Systematic Investment Plan or SIP is a smart and hassle free mode for investing money in mutual funds.

Planning your taxes is an integral part of your financial planning. Sec 80C of the Income Tax Act allows you to claim deductions upto 1.50 lakhs...

Continue Reading

Great Warrior needs a coach! Even God of Cricket needs a coach...

Don't spend too much time on deciding where, how and when to invest. The faster you invest money,

the more it earns.

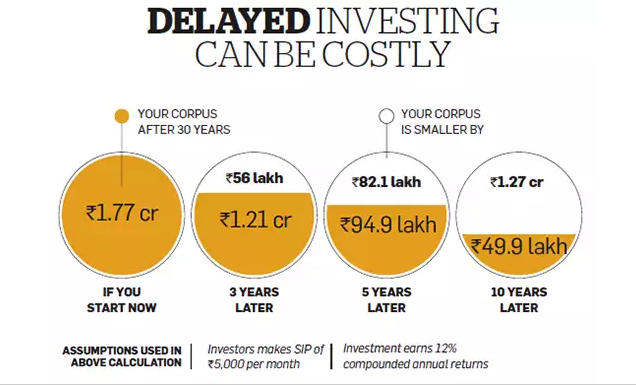

A delay in making an investment can lead to a loss. The accrued interest on the investment for the

duration of the delay can have a significant effect on the net returns.

If an investor starts an investment of Rs 5,000 in a fund that gives 12% returns, he will accumulate Rs

1.77 crore in 30 years. But if he delays his investment by just 3 years his corpus will be Rs 1.21 Cr,

smaller by 56 lakh.

Many young earners don't start investing because they believe their income is low & they can start

investing later. But this is not true. With the passage of time, Individual responsibilities grow & his ability

to take risk gradually decreases. If invested late when the risk appetite lowers due to the newer

financial goals and other responsibilities, Individual investments may get overshadowed.

An Investor can Start Investment with the amount he is comfortable with, with the passage of time one

can increase the investment amount.

A Systematic Investment Plan or SIP is a smart and hassle free mode for investing money in mutual funds. SIP allows you to invest a certain pre-determined amount at a regular interval (weekly, monthly, quarterly, etc.). A SIP is a planned approach towards investments and helps you inculcate the habit of saving and building wealth for the future.

A SIP is a flexible and easy way to plan investment. Your money is auto-debited from your bank account and invested into a specific mutual fund scheme. You are allocated certain number of units based on the ongoing market rate (called NAV or net asset value) for the day.

Every time you invest money, additional units of the scheme are purchased at the market rate and added to your account. Hence, units are bought at different rates and investors benefit from Rupee-Cost Averaging and the Power of Compounding.

Most investors remain skeptical about the best time to invest and try to 'time' their entry into the market. Rupee-cost averaging allows you to opt out of the guessing game. Since you are a regular investor, your money fetches more units when the price is low and lesser when the price is high. During volatile period, it may allow you to achieve a lower average cost per unit.

Albert Einstein once said, "Compound interest is the eighth wonder of the world. He who understands it, earns it... he who doesn't... pays it." The rule for compounding is simple - the sooner you start investing, the more time your money has to grow. With a small contribution on a monthly basis, investor can accumulate a large corpus & can achieve their desired objective.

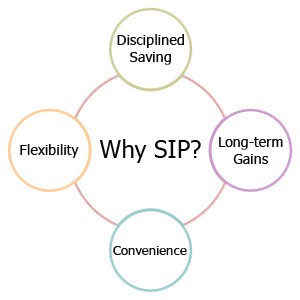

1. Disciplined Saving - Discipline is the key to successful investments. When you invest through SIP, you commit yourself to save regularly. Every investment is a step towards attaining your financial objectives.

2. Flexibility - While it is advisable to continue SIP investments with a long-term perspective, there is no compulsion. Investors can discontinue the plan at any time. One can also increase/ decrease the amount being invested.

3. Long-Term Gains - Due to rupee-cost averaging and the power of compounding SIPs have the potential to deliver attractive returns over a long investment horizon.

4. Convenience - SIP is a hassle-free mode of investment. You can issue a standing instruction to your bank to facilitate auto-debits from your bank account.

SIPs have proved to be an ideal mode of investment for retail investors who do not have the resources to pursue active investments

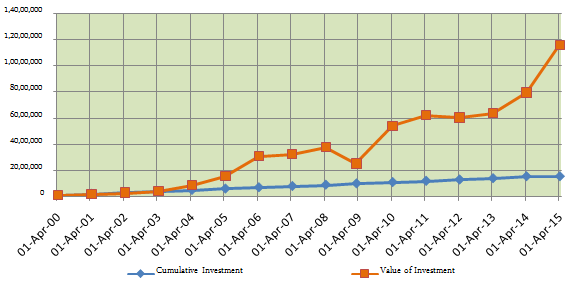

If you have invested 1 lakh rupees every year in PPF & ELSS scheme, after 15 years your valuation in PPF account would be 30.32 lakh, whereas ELSS valuation would have been grown to whooping 1.20 Cr.